This summer, my husband, Jeff, and I traveled to Glacier National Park. One of our reasons for going was we wanted to see the glaciers before they melted. The photo above is us at Grinnell Glacier on the east side of the park. As you can see, it’s a little soupy around the edges. By most predictions, it and all of the other glaciers will be gone within ten to fifteen years. The Social Security Trust Fund is in a similar state. If nothing is changed, the trust fund will be gone inside of twenty years.

According to the 2016 Trustee’s report, the fund backing Social Security Disability Income payments will be exhausted by 2023, and the fund backing Old Age and Survivor Insurance (what we usually think of as “Social Security”) will be exhausted in 2035. The two are separate, and by current law one cannot be used to pay for the other. Yet most analysts implicitly assume the Social Security trust will be tapped to fund disability payments, bringing the projected life of the two together to 2034.

The Trust Fund balance is declining because benefit payments are growing by more than what tax revenue and interest earnings can cover. That requires the use of the Fund principal to make the payments. The principal is the accumulation of all previous tax collections and interest earned after benefit payments. The following chart, showing income from taxes and interest minus benefit payments, illustrates the problem. The declining slope of the line means that benefits are higher than income.

The two funds help support 60 million people; 43 million retired people and their dependents, 6 million survivors of deceased people and 11 million disabled people. In 2023 when the Disability Income Fund is depleted, the tax revenue supporting the program will only be able to pay 89 percent of the benefits, and in 2035 when the Old Age and Survivor Insurance Fund is depleted, the tax revenue will only support 77 percent of projected benefits. In order to solve the problem, an immediate tax increase of 2.6 percent or an immediate reduction in benefits for all current and future beneficiaries of 16 percent (or some combination of the two) is necessary.

This isn’t what was intended when Franklin D. Roosevelt first considered creating a social insurance program in 1934. FDR envisioned a self supporting system, similar to an insurance contract, where contributions for a worker would be collected over his or her lifetime and invested. The contributions and investment interest combined would provide the funding to pay out the worker’s benefit at the end of their work life.

Of course this wasn’t possible in the early years of the program, because it would be decades before a worker would have contributed enough for a fully funded benefit. Therefore the early payments had to be funded from the contributions of those still working. The new law included a schedule of tax increases to be implemented over time to make the program self-funding. Without the tax increases, the system was projected to require government subsidization by 1980.

When Social Security was implemented the benefit payments were cheap relative to the tax revenues that were being collected. In 1940, there were more than 159 workers for every beneficiary. As a result, congress didn’t see any harm in pushing the tax increases back as well as expanding the program. But by the mid-70’s the system was running out fo money. Since then, there have been changes to the retirement age and increases in taxes to shore up the funds, but they haven’t been enough to over come the rising tide of retirees.

By 1955, the ratio of workers to beneficiaries had fallen to just under 9 and ranged between 3 and 4 from 1970 to 2009. Now the ratio is less than 3, and by 2035 it will be just over 2. The reluctance to increase taxes combined with the eagerness to expand benefits have created a pay as you go system with too few left to pay.

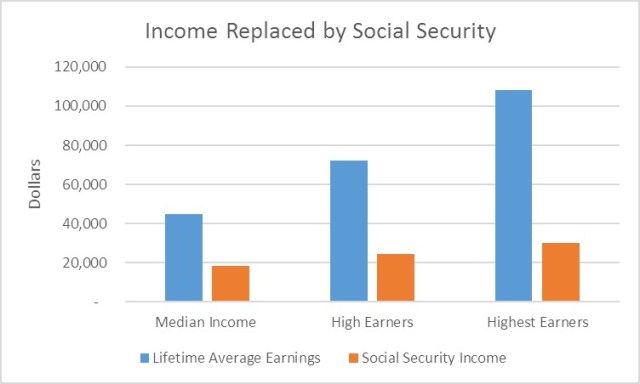

Social Security is already a poor substitute for a retirement income. Benefits represent a fraction of the income earned by the typical working individual. Based on current benefit calculation methods, for those with median lifetime earnings, social security will replace about 41 percent of those earnings. For the highest earners the ratio is just over a quarter. If benefits are cut due to inadequate tax revenue, Social Security will replace less than a third of average earnings for those with median income levels and only a fifth for those with the highest income levels.

There are no current proposals on the table to reform the system. The Trust Funds will continue to melt away, just like the glaciers. While the demise of the Trust Funds won’t mean that Social Security will go away, it could provide even less support than it does today. With little hope that Social Security will be shored up, saving to fund your own retirement has to be a priority. Without savings, Social Security alone will not even provide for basic living expenses. It is never too late to start saving. Take stock of where you are, set a savings goal and make what you can of the time you have in the work force.