Do you work with an investment adviser?

How often do you meet with your adviser?

What do you talk about beyond the investments?

What are you paying for your advice?

Unfortunately, for too many people who answer yes to the first question, particularly those with small balances (less than $1 million), the remaining answers are never, nothing and I don’t know.

Over the last several months I’ve reviewed a number of investment portfolios for people who work with advisers. Sometimes it’s good to get an unbiased second opinion, especially if it is free and not given with the intention of winning business. In general, the investment strategies have been just fine, but what has caused me concern is the high fees combined with a lack of service.

In one account, the adviser was charging what seemed to be a relatively low annual fee of 0.60 percent of assets under management (about $6 per $1,000), but he was investing the money in class A shares, which not only had high internal expense ratios, but also had a front end load of 3.50 percent. The internal expense ratio is what the mutual fund manager gets paid to manage the mutual fund. The front end load is paid to the adviser for selling the mutual fund to you. The investor was depositing $1,000 per month, and every month’s deposits were being hit with the 3.50 percent load. That was in addition to the management fee. Average expenses were nearly 2.0 percent per year on the account.

What was the adviser doing for this compensation? Nothing. The owner had never met the guy. He had taken over the account from the previous adviser who no longer worked for the firm.

In another case, a friend left one adviser because he didn’t think his investments were doing as well as they should have been. He moved his investments to an adviser at his credit union. The new adviser charged a 1.0 percent per year management fee and invested the money in a variety of mutual funds. All of the mutual funds had above average internal expenses, making total expenses close to 2.0 percent again. At least in this case, my friend had met with the adviser. But only once. There was no financial planning. There was no assessment of estate planning needs. There was not even any subsequent review of the investments.

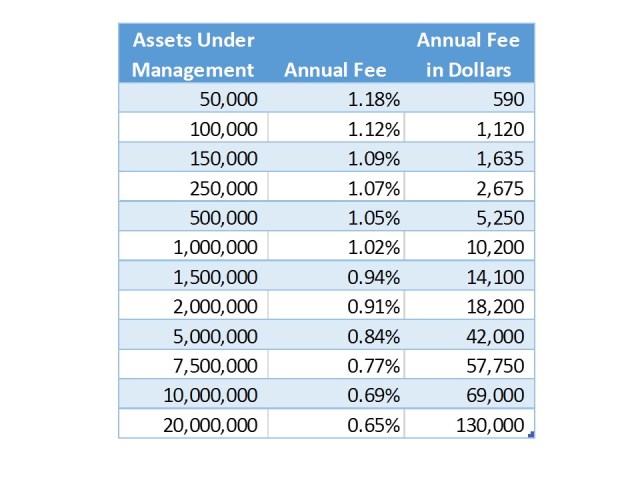

Below is a table showing the average investment advisory fee charged by a sample of advisers nationwide from a survey conducted by Advisory HQ. If your portfolio is less than $1 million it is pretty typical to pay an adviser at least 1.0 percent. These fees don’t include any investment expenses, which could increase total expenses a little or a lot depending on whether the adviser uses cheap index funds or expensive actively managed funds.

Advisers need to make a living and smaller accounts just don’t pay for themselves. Some advisers work on an hourly fee, but most don’t like to do that. There is no leverage in that fee model. The adviser can only make as much as she has hours in the day. Most advisers work on a percent of assets under management structure, where their income can grow with the amount of assets they manage. But that means advisers have an incentive to work with larger accounts. An adviser can make almost as much money with one $1 million account as she can with ten $100,000 accounts.

In order to make small accounts work for advisers, they often streamline the service model. If your account is small, you may see your adviser less often than larger accounts do. Your service may be limited to investment management, which will include creating a portfolio of mutual funds. The adviser will review your investments regularly and maintain the portfolio structure over time, though they may not speak with you very often. If that is all you are getting, you can do just as well for a lot less money.

Enter robo-advisers. The very name seems derogatory. However they are a great solution for people who aren’t getting much service from their current human adviser. Robo-advisers use automated systems to create an investment portfolio for you based on your investment objectives, time to meet those objectives and other information designed to gauge how much investment risk you can take without running for the exits.

These advisers generally use low cost exchange traded index funds or index mutual funds, so the investment expenses are low. Because the investments are maintained automatically, there is no human to pay, and therefore the fees charged by the advisers are low too (some are even free). That leaves more of your investment return for you.

Two of the top rated robo-advisers are Betterment and Wealthfront. Betterment offers investment management using exchange traded funds from 12 different investment categories. Fees for service are tiered and range between 0.15 percent for accounts with more than $100,000 invested and 0.35 percent for accounts with less than $10,000 invested. There is no account minimum. Average investment expenses are just 0.13 percent. For a $100,000 account, you would pay just $380 per year all in. That is $210 less than the average human investment adviser’s fees alone, without taking the investment expenses into account.

Wealthfront offers a similar service. They use exchanged traded funds from 11 different investment categories. They charge no fee for the first $10,000 and then charge 0.25 percent for higher balances. Their investment expenses are about 0.12 percent per year. Annual expenses on a $100,000 account would be about $345. Nerd Wallet has done a good review of several different robo-advisers that is worth checking out.

Robo-advisers are registered investment advisers that take fiduciary responsibility for their clients’ accounts. Fiduciary responsibility means they are required to invest in their clients’ best interest. However they have been criticised. The main concerns are that they can’t offer advice on money they aren’t managing, because the systems simply can’t see it, and the information gathered by questionaires may be too shallow.

If you aren’t getting a lot of service from your adviser, he isn’t in any better shape than a robo-adviser. If you have an account he doesn’t manage, like your 401(k), your investments with your adviser and your 401(k) investments may not come together in a cohesive investment strategy. Human advisers tend to tout the advantages of their customized approaches, but unless your advisor is meeting with you regularly, his investment strategy will be based on limited information too.

The primary driver of investment strategies in general is your time horizon. Your time horizon dictates how much risk you can reasonably take, and therefore how much of your investments should be in risky stock market investments versus lower risk income oriented investments. Time horizon is something that can reasonably be collected through an electronic questionaire. I’ll bet your adviser had you fill in that information on a form when you opened your acount.

A good adviser is worth the money that you pay. A good adviser will help you with saving as well as investing. She will meet with you regularly and take into account all of your investments, even the ones she doesn’t manage. She will advise you on how to put an estate plan in place, how much insurance you should own and how to manage your tax burden effectively. She’ll help you understand what you need to retire, and how long it will take you to get there. If you are getting this kind of service, 1.0 percent of assets under management is a reasonable fee. It is low if your account is less than $1 million.

If you are not getting this kind of service, 1.0 percent is way too expensive. If your adviser isn’t going to do more than put together a few expensive mutual funds for you and send you a statement once a quarter, you shouldn’t be paying him so much. All you are getting is a faceless automated solution. A robo-adviser will do the same thing for a lot less money.

Image courtesy of iosphere at FreeDigitalPhotos.net

One thought on “Robo-Advisers Can be Better than Human Advisers for Small Accounts”