The housing market in many areas of the country has seen dramatic increases in prices over the last five years. Home prices in coastal metro areas, like Portland, seem to be on fire. If you don’t already own a home, your hopes of buying one may be dimming as each month brings higher prices. It takes time to save up for a down payment, especially with today’s housing prices. Should you take the money you’ve stashed in your retirement savings and use it to buy a home?

Using the S&P/Case Shiller 20 City Composite Home Price Index, home prices have risen, on average, nearly 8.0 percent per year since the bottom of the housing market in 2012. The fast pace of price increases was at least partially due to the depths of the decline in the market. Since the last peak in housing prices in 2006, nationwide home values are still down. Longer term, home price appreciation has been much more modest. Nationwide, since 1980, home values have only increased 3.6 percent per year. Even in trendy Portland, prices are up just 4.7 percent per year. So values are unlikely to continue to run at the pace of the recent past.

Still it’s hard to not want to jump in for fear of being priced out of the market altogether, especially if you have enough money for a down payment sitting in your retirement account. But raiding that account is not the answer.

Depending on the account type there are limitations to what you can do. If you withdraw your money from a traditional 401(k) or IRA, you will have to pay taxes on the balance you take out, and you may also pay a tax penalty. You could borrow money from your 401(k), but you can only borrow the lower of $50,000 or half of your balance.

If you have a Roth IRA, you can withdraw your contributions at any time, however if you withdraw earnings on your contributions before age 59½ you will pay both taxes and a penalty. Roth 401(k)s have similar rules, plus many employer plans limit withdrawals while you still work for your company, though loans are still an option.

If you take a loan from your 401(k), you will make monthly payments, and those payments are not considered contributions to your plan. So, unless you make a contribution and a loan payment, you will miss out on the employer match if your company offers one. Loan interest is paid to you, but the interest rate is generally lower than the return you can expect from growth oriented investments available in your plan. And if you leave your job before the loan is paid, you will have to repay the loan in full or pay taxes and penalties as if the loan were a distribution.

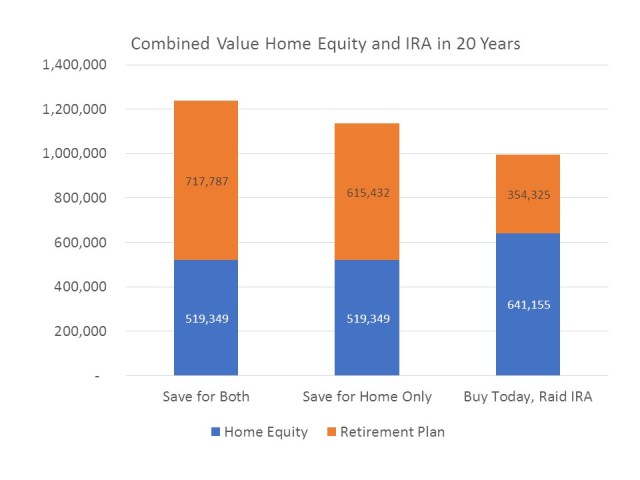

Let’s say you have the best situation possible. You have a Roth IRA account with a balance of $100,000, and you can withdraw enough to cover your down payment without triggering taxes. You have three choices. You can continue to save in your Roth IRA and at the same time save for a down payment for your home. You can stop making your Roth IRA contributions and use the money to add to your savings for a down payment on a home, or you could withdraw the down payment from your Roth IRA.

With option one, your retirement account will continue to grow as before. But the cost of the home you want to buy will continue to rise, and given how low interest rates are today, you will likely pay higher interest on your mortgage loan. With option two, your balance won’t grow quite as fast, because you aren’t adding money to your account. With option three, you buy today with a down payment withdrawn from your IRA. You put a big dent in your retirement savings, but your home price will appreciate and you can lock in today’s low interest rates.

To figure out which option is best, I’ve calculated the combined retirement plan balance and home equity twenty years from now using some assumptions. I’ve assumed home values will increase on average 3.6 percent per year for the next 20 years, but over the next five years they grow at a somewhat faster pace of 4.0 percent per year. Using a modest home in my neighborhood (1,100 sq ft) as an example, today’s purchase price is $390,000, but in five years, the same house would be valued at $474,000. Today’s 30 year mortgage rate is 4.25 percent, and I’ve assumed rates rise to 6.25 percent over the next five years.

I’ve also assumed that you would ordinarily save $5,500 (the maximum for 2017) per year in your IRA. The average annual return on your IRA investments over the next 20 years is 8.0 percent, because you are still young and investing primarily in stocks. The following chart shows the results.

In option one and two, you put off buying the home for five years while you save up the down payment. In option one you are able to save for both. In option two you opt to not add to your IRA, but you don’t take anything out either. In both cases you pay a higher price for the house and higher interest rates, because you have to wait five years. In option three, you take out enough from your IRA to cover the 20 percent down payment on the home today, leaving you with about $22,000 in retirement savings.

You do have more home equity in option three, but your retirement account has taken a nasty hit. The value is only half what it would have been if you hadn’t touched the balance and continued to make the contributions. Even if you stopped contributing to your IRA while you save for a down payment, you would be better off than if you raided it today.

To raise a down payment for the house in question, you would need to save about $19,000 per year to be able to buy it in 5 years with the assumptions I’ve made. To recover from raiding your IRA, you would need to save the same amount above your normal $5,500 contribution over nine years, or $171,000 instead of $95,000.

As tempting as it might be to use the savings you’ve already built for retirement for a down payment on a home, in the end you won’t come out ahead. You need that balance to grow for you as long as possible. Dipping into those savings takes valuable time away from growing your account. As hard as it may be, you will still be better off saving for your home, even in the face of rising prices.

Image courtesy of fantasista at FreeDigitalPhotos.net

Does it take into account the money you would spend if you continue renting a similar size house? And is this applicable to the current covid-19 situation?

LikeLike

That is a good point. The calculation does not take into account the fact that while you are saving a down payment you are also paying rent. But it also doesn’t take into account that owning a home generally costs more than renting. With home ownership you also have to pay for property taxes, insurance and maintenance, which can be quite expensive. The big difference today from when this article was written is the fact that you are temporarily allowed to withdraw $100,000 from your 401k. You would still pay taxes on the withdrawal, but there is no early withdrawal penalty. However, if you take that withdrawal, it will take a long time to replace it and the earnings it would have generated.

LikeLike