Every year after Halloween, time begins to accelerate as the year hurtles through the holidays and to its eventual end. But before you brace yourself for the feasts and family, you have some business of your own to take care of. For most employers, November 1st marks the beginning of open enrollment for company benefits.

While the centerpiece of open enrollment is healthcare benefits, its also a good time to pay some attention to your retirement account. You should revisit your contributions and your investments, consider switching your contributions to a Roth option and update your beneficiaries.

Contributions

Your minimum contribution should be enough to get your company’s match. Most employers require you to contribute 6.0 percent to get the full company match. If you are contributing the minimum, you aren’t saving enough for retirement. Make an effort to increase your contributions this year, and each year from here on out, until you hit the maximum.

The 2018 contribution limits for employer sponsored retirement accounts, such as 401(k)s, has gone up. It is now $18,500 and if you are over 50, you can contribute up to $24,500. If your goal is to contribute the maximum to your account, you may need to adjust your contributions.

Rebalancing

With the stock market up, you may find that you have more money in mutual funds investing in stocks than you intend. Now is a good time to sell some of your stock market investments and buy more conservative investments to rebalance your account to its target allocation. If your company’s plan offers an auto rebalancing feature, where your account could be automatically rebalanced to its target allocation, now would be a good time to turn it on.

Not sure what your allocation should be? Most plans offer help with figuring this out, whether its through planning tools available on the web site or some form of professionally managed investment option.

In the professionally managed category, target date retirement funds are now widely available. You can tell which ones these are, because they have a year in the name of the fund, such as target retirement 2045.

Target date funds are fully diversified investment options. The fund’s manager gradually reduces the fund’s allocation to risky stock market investments as the target date approaches. All you have to do is select this investment option, and your retirement account will be managed in a reasonable way for your age and the time remaining before you stop working.

If your company’s plan doesn’t offer target date retirement funds, they may offer a managed account option. With a managed account option, your investments will be managed for you by an investment adviser based on information you provide, usually through an on-line questionnaire.

If none of these are available to you, one easy rule of thumb is to subtract your age from 120 and invest that percentage in stock mutual funds. Then invest the rest in bond funds.

Roth Accounts

Now is also a good time to check whether your company offers a Roth retirement account option. Both accounts allow your investments to grow tax free while you are saving for retirement, but they differ in the tax treatment on both the front and back ends.

With a Roth option, your contributions are after tax, whereas with a traditional account, your contributions are before tax. While the before tax contributions make the traditional accounts appealing on the front end, Roth accounts have more advantages on the back end, when you are withdrawing your money.

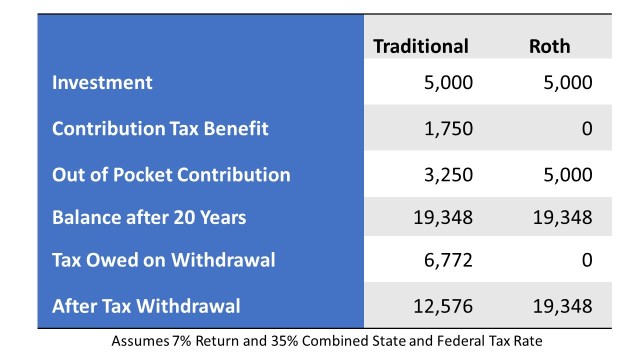

When you want to spend your money in retirement, withdrawals from a traditional account will be fully taxable, while withdrawals from a Roth account will be fully tax-exempt. The following table shows the advantage of the Roth account over a traditional account with a single year’s contribution.

Because the growth in your investments will be far greater than your contributions, your tax bill on withdrawal from a traditional account will be higher than the tax advantage you gained on deposit. That makes the Roth option, with no tax obligations on withdrawal, more attractive.

Roth accounts have other advantages. You can withdraw your contributions, though not your earnings, at any time without paying taxes. This comes in handy if you plan to retire before you are 59 ½. You also won’t be required to take a minimum distribution when you turn 70. Finally, withdrawals from a Roth account are not included in your income calculation for determining whether your social security benefits are taxable.

Anyone can contribute to a Roth retirement account through work. There are no income limitations as there are with Roth IRAs. If your employer matches your contribution, they will match your Roth contribution by making a contribution to a traditional account. So you will wind up with two retirement accounts through work.

If you move your balance in your traditional account to the Roth account you will be taxed on the amount transferred, so don’t do that unless you’ve checked with a tax professional and know what you’re in for. However, your future contributions can go toward a Roth account.

Beneficiaries

Review your beneficiaries. Regardless of any other documents you may have, such as a will, financial institutions rely solely on your beneficiary designations to distribute your account in the event of your untimely demise.

If your spouse has changed, make sure your prior partner is not still your beneficiary. Do not make minor children beneficiaries, because financial institutions cannot distribute money directly to them until they turn 18. Consider establishing a family trust, and making it your beneficiary, to allow your children’s guardians easier access to the money needed to raise your kids.

There is no time like open enrollment to focus your attention on financial matters. Before things get hectic with the holidays, take advantage of this annual checkpoint to make sure you are on the right track with your retirement benefits. Your work related retirement plan may well make up the bulk of your retirement savings, so take advantage of what is available to you.

Image courtesy of David Castillo Dominici at FreeDigitalPhotos.net

Hi, Julie. Thanks for the information. While I agree that a Roth 401(k) is usually better than a traditional 401(k), I think your example may overstate the financial advantage. In the example, a $5,000 Roth contribution in a 35% tax bracket will mean that the taxpayer’s tax bill at the time of the conrtribution will be $1,750 higher when compared to a $5,000 contribution to a traditional 401(k). A better comparison is to compare a $5,000 Roth contribution to a $6,750 contribution to a traditional 401(k) plan. In that case, the 401(k) balance at year 20 for that single contribution at a 7% return will be $26,120 and the tax bill at 35% will be $9,142, leaving $16,978. So, the Roth approach is still better, but not as dramatically. The traditional approach may be better in situations where the higher contribution by the employee leads to a higher match by the employer or the participant expects to be a lower tax bracket at retirement. One advantage to the Roth is that, if the Roth 401(k) is transferred to the Roth IRA after retirement, then the Roth IRA can be inherited with the same tax advantages to the recipient. Finally, while 401(k) plans may allow conversions to a Roth account within the 401(k) plan, not all plans allow these conversions, sometimes due to systems limitations of the 401(k) plan administrator.

LikeLike

Thanks Kim.

LikeLike