Welcome to 2018. Now that the Christmas decorations are put away, the champagne has been sipped and the resolutions made, it is time to get down to business. If one of your resolutions was to pay down your credit card debt, there is a tool you may not have considered that can give you a leg up. It’s another credit card.

No, I usually don’t endorse opening new credit cards. You’ve got enough trouble with the ones you have. However, if you are truly committed, a card where you don’t have to pay interest will juice up your debt reduction efforts for any payment amount you intend. The reason is more of your payment will go directly to reduce your balance and less to interest.

Some credit cards offer a balance transfer feature with a zero percent interest promotion for the first 12 to 21 months, depending on the card. If you transfer your balance from another high interest card, you won’t incur interest during that promotional period. That means your entire payment will go to pay down your balance.

The cards generally have a 3.0 to 5.0 percent balance transfer fee. But compared to the high average annual rate charged on a typical credit card, it may be well worth it.

A survey done by U.S. News and World Report, found that most credit card holders who carry a balance had not used zero interest credit cards to reduce the cost of their debt, and two thirds thought they could pay off their balance within 18 months, a typical promotional period.

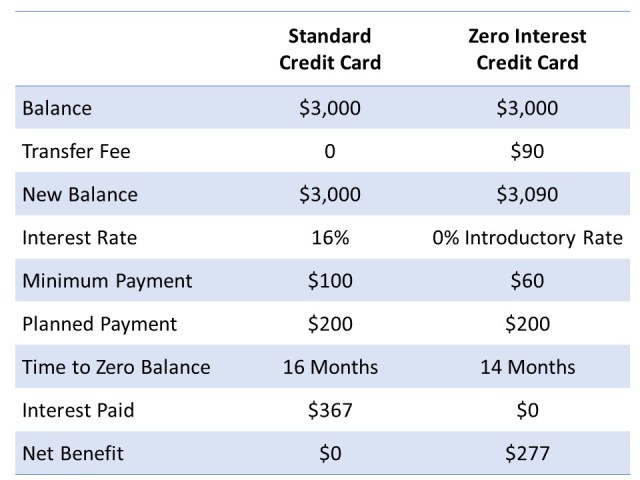

The following table shows how transferring a $3,000 balance from a typical credit card, with a 16.0 percent interest rate, to a card with a zero interest introductory rate could save you money and get you out of debt faster. With a $200 monthly payment, the balance is paid off two months earlier on a zero interest card, and you save $277 in interest, after the balance transfer fee.

There are some pitfalls, and not all cards are created equal. The first area of concern is which transactions get the zero interest treatment. For some cards, it is only new purchases, and for others it is only the balance transfer. Since you are trying to reduce your debt, you want zero interest on the balance you transfer.

Avoid making new purchases on your card. If you make additional charges, it can hamper your debt reduction efforts. When a card charges different interest rates on different transactions, regulations require payments above the minimum be applied to the balance with the highest interest rate. That means your extra payments will pay off your new purchases before they go to pay off the balance you are working on.

The financial institutions issuing these cards have no mercy when it comes to late payments. If a payment is late during the zero interest period, you may lose the zero interest benefit, and your rate will bounce up to the current new purchase rate. As a result, you will have paid the transfer fee for no reason.

Finally, if you are unable to fully pay off the balance you transferred within the promotional period, you may have to pay deferred interest on the balance remaining. That means your remaining balance will be charged the new purchase interest rate for the full introductory period at the end of that period.

U.S. News has a good comparison of the top balance transfer cards. In addition they provide a more in-depth guide to determining whether a new credit card is the right move for you.

Before you embark on this debt reduction mission, make sure you are working on the right priority. Debt reduction is not the first step on your road to financial security. Your emergency fund is. Don’t make extra payments on your debt until you have built up at least three months of living expenses in savings.

Debt reduction should also wait until you can manage it as well as a contribution to your company retirement savings plan large enough to get the company match. The company match is free money. Or, put another way, it provides a 100 percent return on your contribution. Debt reduction saves you a lot, but not nearly 100 percent.

Eliminating your high interest credit card debt is an important goal. If you have an emergency fund in place and you are getting your full company match in your retirement savings plan, it is the next thing you should be working on. Taking advantage of a zero interest credit card, can make your efforts even more effective. For at least a short time, your payments will go directly and fully to reducing your balance.

Image courtesy of adamr at FreeDigitalPhotos.net

Once again, an excellent article by Julie!

LikeLiked by 1 person