With school having just started, many homes with teenagers are starting to get serious about preparing for college. Some seniors will be taking early acceptance by November, while juniors are mulling their options. So it’s time to get real with your kids about how you’ll pay for college.

You want the world to be your child’s oyster, and no one wants to talk about expenses when dreaming about the future. College is expensive no matter where your child chooses to go, but some choices will set you back farther than others. The following chart shows the average cost of college for the 2017-2018 school year from the College Board.

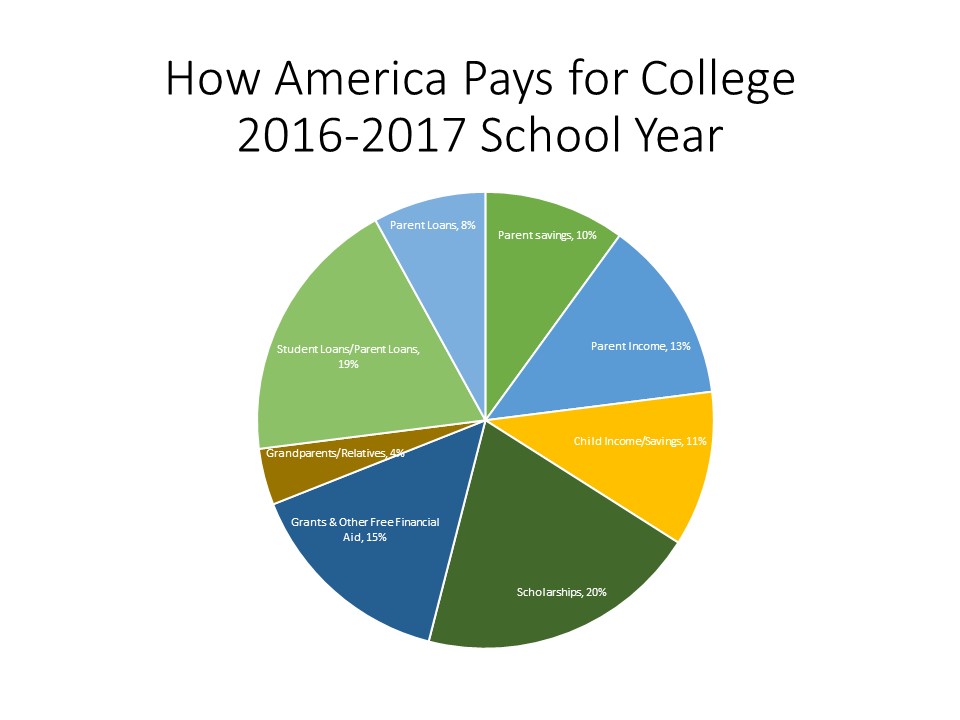

While most parents want to send there children to college, only about 57 percent of them save for it. The average household savings for college was only $18,135, according to Sallie Mae. That won’t even cover a single year at a four year school. So, that means the money must come from somewhere else. The following chart shows how America pays for college, also from Sallie Mae.

A full 27 percent of the cost of college will be paid for with loans. The average student loan debt per borrower from the class of 2017 was $28,650. At the current Federal Direct unsubsidized student loan interest rate of 4.53% for undergraduates, over the standard 10 year repayment period, payments on loans of that amount will be about $297 per month.

That can be a significant piece of a new graduate’s entry level job income. It’s no wonder that 30 percent of college graduates with student debt move back in with their parents. With money like this on the line, it is important to sit down with your future college student and cover the facts.

Here are five things to discuss with your child before she chooses a school.

- Tell your student how much you will be able to pay. This includes what you have saved and what you are willing to commit to out of your income. The converse of this is how much should she expect to pay.

- Outline options for raising the extra money. In addition to student loans and scholarships, your student may be able to raise some money through part-time or full-time work. Taking a gap year to work and save up for school is a reasonable approach.

- Help your student understand the implications of their choices. Private and out-of-state public four year schools cost nearly twice as much as in-state public institutions. Student loans may be hard to avoid, but they can certainly be minimized if you understand your trade-offs. You can calculate the monthly payments given different loan amounts on the Federal Student Aid web site.

- Provide context for the information. Estimate the kind of monthly salary your student might earn given her career interests. Payscale’s College Salary Report is a good place to start. It wouldn’t hurt to also talk about average living expenses. Nerd Wallet has a cost of living calculator. Don’t forget to show the impact of taxes. How much of her take home pay will be left after student loan payments?

- Consider starting school at a community college. The average cost per year at public two year colleges is only $3,570 assuming your student can stay at home while she attends.

If you don’t have enough saved to pay for college, think carefully about the impact of paying for school out of your current income. It can put you behind in your efforts to save for your own future. And avoid taking on your own debt to pay for college for the same reason. If you are behind in saving for your own retirement, paying for college should not be your top priority. Your child has time to recover from the expenses of school. You do not.

A college education can substantially improve your child’s ability to earn a living. But taking on a lot of debt to pay for it can weaken her financial stability. Help her understand that her choices have implications for her lifestyle after school. Before she makes her final decision, she should know what she’s in for.

Save Yourself; Your Guide to Saving for Retirement and Building Financial Security, is available on Amazon.