I’ve been asked more than a few times whether rental property was a good investment. Many people feel more comfortable with an investment they can go and visit than with the stock market which seems so out of our direct control. When a duplex went up for sale near us, it seemed like a good time to do an analysis.

A good investment is one that provides you a good return for the risk that you take. Of course good and risk may be in the eye of the beholder and depends to some degree on how long you expect to hold the investment. For comparison, we’ll use the return on the S&P 500 and it’s range of historical returns over ten year periods to gauge the return on this rental property.

What should be included in our analysis? Well of course we’ll include our annual rent and an estimation of the increase in the value of the property. But we’ll also need to subtract the costs involved in owning the property. Those include property taxes, insurance and maintenance. If we take out a mortgage to buy the property, we’ll also need to include the interest on the loan. Finally we’ll need to make an assumption for inflation on both the income and expense side.

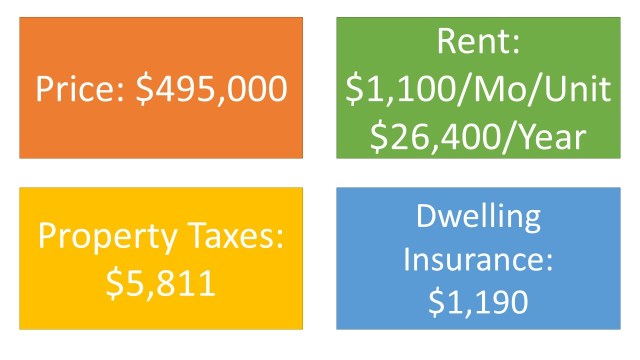

The duplex that is for sale has two 1,000 square foot, two bedroom, one bath units. Here are the reasonable expectations for this property here in Portland.

There are two rules of thumb about what to assume for maintenance costs. One suggests using 1.0 percent of the purchase price, and the other suggests using $1 per square foot. The property for sale was built in 1957 and likely could use some tender loving care. So I’ll take the higher of the two and use $4,950 per year as an average maintenance cost estimate. That puts our net annual rent, after expected expenses at $14,449. If we were to take out a 30 year mortgage to buy the property*, deducting the interest cost would leave $710 in annual rent. That’s not much, but property values tend to increase over the long run. Will the increase in value provide our return?

Using data from the Federal Housing Finance Agency the following chart provides the average annualized rate of increase in home prices over different periods within the 1991 to 2016 time frame. The Portland market data is from Zillow.

As you can see, the Portland market has been hot, but the increases in prices over the last five years here are not sustainable. The best ten years nationally, at 6.8 percent, ended in 2006 and there is not another period with price increases of that magnitude. So we’ll exclude those two data points. The last ten years were also an anomaly. The price declines from 2006 to 2011 were the worst in the 1991 to 2016 time frame. A reasonable assumption for the increase in the future value of our property would be the longer term national average annual increase of 3.4 percent.

A few other assumptions can go into our analysis. Rents and property taxes go up more or less with inflation, so I’ll include an annual 2.0 percent increase in these values as well as the cost of insurance and maintenance. With all of this information what is our expected investment return?

While the price of the property is $495,000, if we mortgage the purchase with a 20 percent down payment, our investment is only $99,000. The mortgage leverages our return, so our net rent and price increases would be judged on that basis, not $495,000. As we make mortgage payments the base does grow, however. Given these assumptions the expected average annualized return over a ten year holding period would be 9.9 percent. That is comparable to the historical averages for the S&P 500.The NYU Stern School of Business data set has the average annualized return for the S&P 500 from 1991 through 2015 at 9.7 percent with similar returns for the full data set which goes from 1928 to 2015.

What could go wrong? Well it’s not likely that we’ll be able to rent the property all of the time, but we’ll have to make loan payments every month. If we assumed that we average ten months of rent per year the return drops to 8.6 percent.

It’s possible that we’ll have to put more into the house than our down payment in order to make the rental units comparable to similarly priced apartments in the neighborhood. If we had to put in an extra $50,000, our return would drop to 7.0 percent. Or alternatively we could rent the units for less; say $750 per month. That would drop our return down to 4.9 percent.

Finally our return is sensitive to the gain in the value of the property. If the next ten years were like the worst ten years for residential real estate prices, our return would be 1.8 percent. If everything works against us, we need to put more money in, rents aren’t as high as we expected and real estate values don’t rise, then we would lose 2.7 percent per year. But if everything works in our favor, we could gain more than 14 percent per year.

The worst ten year period for the S&P 500, ending in 2009, had a loss of 1.3 percent. The best ten year period, ending in 1999, had an annual return of over 19 percent. The same numbers for the full series were also similar.

One other thing to consider is personal effort. While the expected return on a rental property could be in line with what you would expect from an investment in an S&P 500 index mutual fund, the rental property will demand time and attention. An investment in an index fund is passive and requires no effort at all.

So is a rental property a good investment? It’s not a bad investment. In any given time period the return on a rental property could be better or worse than the return on an S&P 500 index fund, a reasonable passive alternative. Over long holding periods, expected returns on a rental property are in line with historical returns on the S&P 500, given the uncertainty of the projections.

Most people will only be able to own one to a few rental properties, and those will be in a single geographic region, which increases the risk of the investment. Rental property requires time and attention. If you value your own time in line with the cost of a property manager, your return would drop further (by about 1.0 percent per year). But if you like the idea of being able to visit your investment, rental real estate might be a good alternative or addition to your stock market investments.

*30 year mortgage loan interest rate: 3.5 percent per bankrate.com.

Image courtesy of fantasista at FreeDigitalPhotos.net