Try this. Figure out how much you spend in a year off the top of your head. Some things will be easy. You know your mortgage or rent payment. You probably have a good idea about what your utilities and other monthly bills run. Groceries might be more of guess. Eating out, gas, car/home repairs, vet bills and other things all also might be harder to come up with, but stick a number on them. Go ahead. I’ll wait.

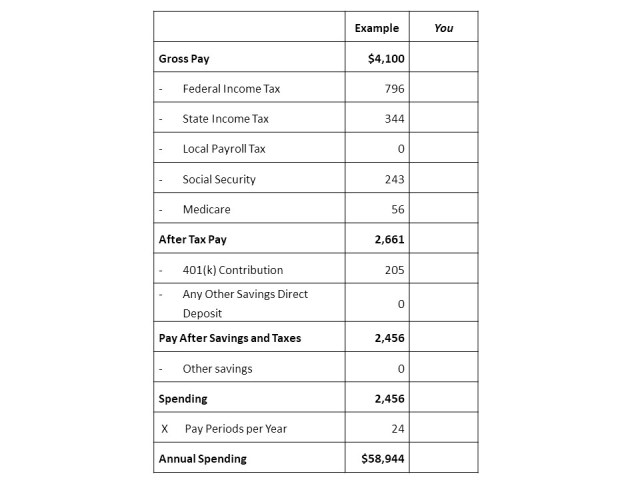

Now, let’s see what you actually spend. Use the following worksheet to calculate your spending from your paycheck.

This is your spending, because it must be. If you didn’t save it or pay it out in taxes, you must have spent it.

Now this might not take into account all your spending. For example, if you usually get a tax refund, and you spend it rather than save it, you can add that to your spending. If you get a bonus that isn’t reflected in your most recent pay, and spend that instead of save it, add that as well.

Are you surprised by how much you spend? Most people that I’ve done this with are. In my small sample of experience, the difference between how much people think they spend and how much they actually spend can be as much as 30 to 40 percent.

Several years ago, my husband, Jeff, and I did this exercise. He couldn’t believe how much we were spending. He was so surprised he committed to tracking all our expenses transaction by transaction for six months. Guess what? Yes, we were spending that much.

Why should you do this? Well to understand how much you will need to save for retirement, you need to know how much you will be spending every year. Therefore it’s important that you have a good estimate. If your estimate is 30 to 40 percent off, you could be in for a surprise. Even if you don’t have a specific plan for how you want to live when you stop working, chances are you don’t want to give up a lot of how you live now, other than the work part, that is.

You can legitimately expect to spend less than you do now in some areas. For example, if you have mortgage or other debt you’ll pay off before you stop working, you can subtract that from your annual spending. If you’re currently paying for college for your children, you can subtract that as well.

But before you go shaving off expenses, you should consider that some of your current costs could be higher when you stop working. You might spend more on travel or hobbies. You could also wind up spending more on health care.

One way to assure that you spend less in retirement is to spend less now, by saving more. If you’re actually spending a surprising amount more than you thought you were, there is a good chance that you are spending your money in ways that aren’t making you happier. The only way to figure that out is by tracking every expense to see where your money is going.

Just gaining the awareness of where you’re spending your money can motivate you to change it. Any expense where you find yourself thinking “I can’t believe I spend that much on…” is a good candidate for a spending cut. You can also force an expense reduction by having more savings automatically contributed to your retirement account. You’re paycheck will get smaller, forcing you to spend less.

Being aware of how much you spend now will help you prepare for your future. Gaining that awareness will also help get your spending under your own control and put you on a path to meeting your financial goals.

Title image courtesy of Stuart Miles and hour glass image courtesy of Sira Anamwong at FreeDigitalPhotos.net