The 2018 Tax Reform bill will have a significant impact on families’ income taxes for 2018. The bill went into affect as of January 1st, and employers received guidance on how much to deduct from employee pay in February. The guidance was designed to line up the new tax rates with the prior withholding tables, so employees didn’t need to file a new form W-4 with their employer.

But you still may want to review your payroll deductions to make sure you are not having too much or too little withheld from your pay. I’ve been waiting to do this post until the IRS withholding calculator was available, and now it is!

According to the IRS, the average tax refund, before tax reform, was over $3,000. That is a lot of money that could be going to build your emergency fund, your retirement savings or to reduce debt if you weren’t paying it to the government. Now, with lower tax rates and a higher standard deduction, your current deductions might exacerbate the over withholding, or in some cases leave you under withheld.

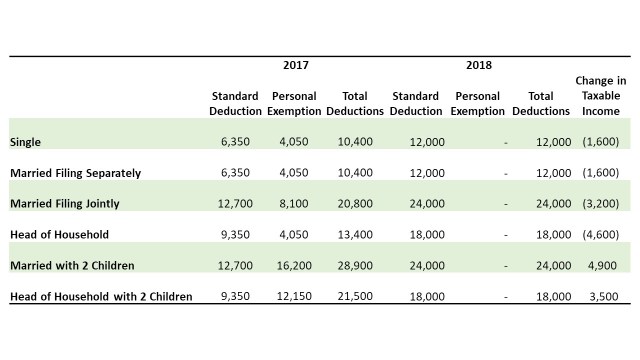

The new tax law increases the standard deduction for everyone, but eliminates the personal exemption. So for many, you will have a lower taxable income due to the increase in the standard deduction, but if you have more than one kid, the loss of the personal exemption will increase your taxable income, unless you have more than the standard deduction in itemizable expenses. The following table provides a comparison.

In addition to the changes in the standard deduction, one of the most common itemizable expenses has been capped. The maximum deduction for state and local taxes is now $10,000. That is high for most people, but if you live in an expensive area, it could raise your taxable income.

Several other common deductions are no longer allowed.

- Casualty and theft losses (unless due to a federally declared disaster)

- Unreimbursed employee expenses

- Tax preparation expenses

- Alimony payments

- Moving expenses

- Employer subsidized parking and transportation reimbursement

The deduction for charitable giving is still available, and the amount you can deduct has been increased from 50 percent of your income to 60 percent. The medical expense deduction is also still available, and the deductible amount is now anything over 7.5 percent of your income, down from 10 percent. The mortgage interest deduction is still allowed as well.

Aside from the changes in the tax laws, you should review your withholding regularly anyway. Things change, and it’s important to have the right taxes taken out of your pay. Not too little and not too much. Too little and you’ll have a tax bill that you didn’t plan at the end of the year, and too much will cost you the opportunity of doing other things with your money.

The IRS withholding calculator will walk you through all the things that should be considered when determining how much taxes to have withheld from your pay. It will estimate the taxes you will owe for the year and the taxes that will be withheld if you don’t make any changes. Then it will recommend the correct allowances to enter on a new Form W-4. To get started, have your most recent pay stub and your 2017 tax return available.

If you have your information handy, the calculator only takes a few minutes to complete. Take a moment and make sure you’re having the right taxes taken out of your pay. If you are like most people, you’re likely having too much taken out and could have more money to put toward your goals if you change your allowances. On the other hand, you can avoid a nasty surprise if the tax law changes worked against you.

Image courtesy of manopphimsit at FreeDigitalPhotos.net