Credit scores are an important number. They will determine whether you can get a loan and how much interest you will pay. They can also determine whether you can rent an apartment, and it is becoming more common for employers to check your credit score before they hire you.

Unfortunately, the credit score carries a lot of mystery and mythology for many. So, in this post, you’ll learn all you need to know about them.

The credit score was invented in the 1950s by the Fair Isaac Corporation. It didn’t catch on initially as a tool, but in 1970, the Fair Credit Reporting Act was passed, which standardized data collection and reporting. The FICO score (from the Fair Isaac Corp initials) gradually gained prominence as a tool for assessing credit worthiness from there.

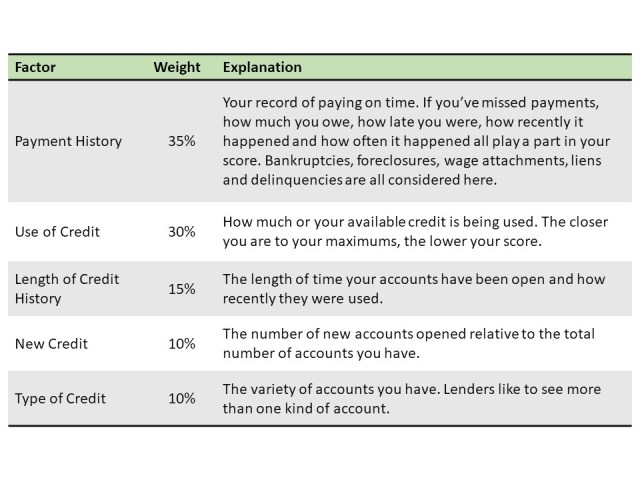

Your credit score has five factors, each weighted according to their importance in determining whether you are likely to repay your loan. The following table summarizes the factors, weights and what they mean.

The biggest factor in determining your credit score is your payment history. So the most important thing you can do to raise your credit score is to make your payments on time. The second biggest factor is how much debt you have outstanding, and the next easiest way to improve your score is to pay down your debt.

Opening and closing accounts can have an impact on your score by shortening the average length of time your accounts have been open, but it will be minor compared to whether your payment history is strong and your balance is manageable.

A friend, who tries to maximize her travel rewards to minimize the cost of travel, opens credit card accounts for the bonus miles and then cancels them once she has what she’s after. She continues to have a stellar credit score, because she always pays on time and never carries a balance. If you have paid off a credit card balance, don’t hesitate to close the account if you no longer use the card.

Checking your credit score has no impact on it. While credit checks to establish new accounts can influence your score under the new credit factor, simply getting a credit report or viewing your score on-line does not change your score.

Regularly reviewing your credit report is an important defense against fraudulent activity in your name. I recently found a credit card account I had not opened on my credit report. Through a little correspondence with the credit agency and the lender I was able to get the account shut down. Debt established in your name is payable by you unless you actively work to close down accounts you didn’t open.

You can actually live without a credit score. If you are committed to living debt free, a credit score is not necessary. Even if you want to get a mortgage, but have no other debt, you don’t need to open some credit card or buy your next sofa on credit to establish a credit history. The things you do all the time will be enough.

If you pay your rent, utilities, cell phone and other bills, on time, and you have a down payment, you have what you need to get a mortgage. However, without a credit score, you may need to work with a smaller mortgage lender and allow more time. The larger lenders like the efficiency of seeing your character summarized in a single number.

Credit unions, independent mortgage brokers, on-line lenders and smaller banks may all be willing to provide the customer service needed to assess your credit worthiness without a credit score. You can get pre-approved before you go house hunting and still be ready to jump on the perfect place when you see it.

You won’t be negatively impacted by having no credit score with other credit checkers. Having no credit score means you have no debt, which is a profound statement these days. Your future landlords will be happy to review your history with prior landlords. Employers looking to judge your character by your credit score will get the information they need by its absence. Certainly no score is much better than a bad one.

Your credit score is an important number, and the best ways to keep it strong are to pay your bills on time and pay down your debt. If you can accomplish that, the other factors play a minor role. You can live without a credit score, so don’t take on debt simply to establish one.

I was wondering the best way to freeze your credit? I don’t anticipate needing to use credit for many years to come and just hate the thought of someone stealing my credit.

LikeLike

Hi Jill, if you visit the credit reporting agencies’ (Experian, Equifax, Transunion) web sites, each one will provide instructions for freezing your report. In the search field for each agency simply type freeze report to find the instructions. It is easy to do, and if you need to lift the freeze later it not hard either.

LikeLike

Another Excellent Article Julie!! Long time reader!!

Someone said to me that paying off credit card balances immediately (versus waiting till the due date) helps? Does this hold any weight?

now if someone could just write one about auto insurance…..

LikeLiked by 1 person